הביטוי "יעילות השיווק" מופיע פעמיים בלבד בתשקיף פייבר (שעליו כתבתי בפוסטים קודמים), ובהקשר השקף הבא:

הגרף מספר למשל, כי סך ההכנסות מקוהורט Q4-17 בתקופה שבין 1.10.2017 ועד 31.3.2019 היו פי 2.1 מההוצאה המכונה "performance marketing" שהוכרה ברבעון Q4-17. מהאמור בעמוד 61 בתשקיף ביחס להגדרת קוהורט שנתי, אנו מבינים כי קוהורט מוגדר על בסיס מועד הרכישה הראשונה (למשל, בקוהורט Q4-17 נכללים כל הקונים שהפעם הראשונה שבה הם ביצעו רכישה הייתה ב- Q4-17).

אליבא דתשקיף, היחס האמור הוא מדד נפלא ליעילות השיווק":

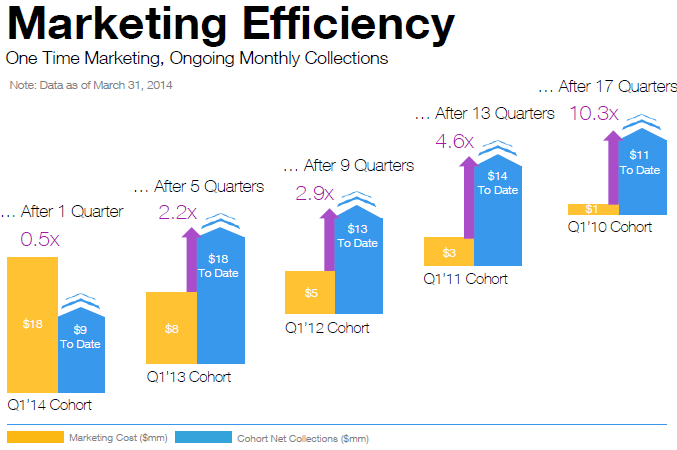

אני משער כי הגרף לעיל והכותרת "יעילות השיווק" צנחו בתשקיף פייבר בהשראת שקף שוויקס מציגה למשקיעים מדי רבעון מאז מאי 2014. השקף הבא הוא ממצגת Q1-14 (כאן):

אבל יש מספר הבדלים בין הגרף של פייבר לשקף של וויקס:

- וויקס לא הציגה שקף כנ"ל בתשקיף או בדוח תקופתי -- השקפים מוצגים רק באתר קשרי משקיעים -- ולכן מעולם לא קיבלה הערות של ה-SEC עליו.

- וויקס מגדירה קוהורט על בסיס מועד הרישום באתר ולא על בסיס המועד שבו נרכש מנוי פרמיום בראשונה. בהגדרה של וויקס אין כל בעיה, אבל ההגדרה של פייבר בעייתית. כך אם אדם עושה חיפוש גוגל לשרותי תרגום בפברואר שבמסגרתו מקליק על פרסומת של פייבר וכך יוצר לה עלות שיווק ופרסום ברבעון הראשון. אבל, בסופו של דבר הוא רוכש את השרות באתר אחר -- ואת הרכישה הראשונה שלו בפייבר הוא יבצע רק ביוני. כך, הוא ישוייך לקוהורט הרבעון השני על אף שעלות גיוסו משוייכת לרבעון הראשון.

- ווויקס מציגה בשקף את המונה ואת המכנה של יחס היעילות. פייבר לא מגלה את מספרי המונה והמכנה בשקף, וגם לא מחוץ לשקף. כך למשל, וויקס מראה שהוצאות השיווק על בסיסן מחושב היחס 2.2 ב- Q1-13 הוא 8 מיליון דולר. כך למשל, פייבר לא מגלה את המספרים מהם חושב היחס 2.1 עבור קוהורט Q1-17.

אף פעם -- משחר נעורי -- לא הרגשתי בנוח עם סוג השקף הזה של וויקס. לפני מספר חודשים, בפוסט קודם. הסברתי מדוע.

סיבה ראשונה: לא בכל השקפים וויקס מבהירה על גבי השקף כי הוצאות השיווק שבשקף נמוכות משמעותית מהוצאות המכירה והשיווק בדוח הכספי. רק בחלק מהשקפים היא מציינת כי הסכומים בשקף לא כוללים "brand marketing expenses". כלומר, סכומי המכנה לא כוללים עלויות פרסום ברדיו, בטלביזיה או במדיה אחרת שאינה אונליין; הם כוללים רק עלויות של "Performance Marketing" -- המשולמות עבור הקלקה או פעולה אחרת של יעד הפרסום.

סיבה שנייה ושלישית: בניגוד לראשונה, שהיא במישור של כותרות נאותות לסכומים המוצגים, הסיבה השנייה והסיבה השלישית עוסקות במהות כלכלית. בפוסט הקודם הסברתי אותן ביחס לקטע שקף ממצגת Q4-18:

סיבה שנייה:

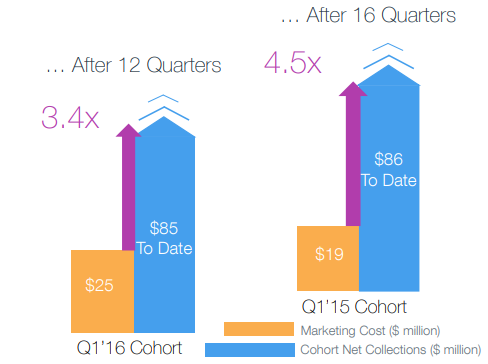

במצגות קודמות, למשל זו מ-Q1/2016, וויקס העירה על גבי השקף, כי ה-$25 מיליון דולר לא כוללים עלות של $7 מיליון לפרסום המותג באותו רבעון (חלק משמעותי מסכום זה, יש לשער, הוא עבור הפרסומת הזו בסופר בול):

לי, באופן אישי, מפריע שוויקס מציגה בשקף השקעה של $25 מיליון ולא השקעה של $32 מיליון, כי הרי ברור שהפרסום בסופר בול הביא הרבה מאד צופי טלוויזיה להרשם באתר ורבים מהם הפכו למנויים משלמים. כך, שאין הקבלה נאותה בין עלות גיוס הקוהורט לתקבולים מאותו קוהורט.

סיבה שלישית:

נניח שמישהו נרשם באתר של וויקס ב-Q1/16 אבל לא עשה כל פעולה נוספת באותו רבעון. נניח שהחליט לעבוד עם אחת המתחרות. ואז בפברואר 2017, הוא צופה בסופר בול בפרסומת של וויקס עם גל גדות ומחליט להתחיל להיות מנוי-משלם בוויקס. כלומר, אותם $25 מיליון דולר של עלות גיוס חברי קוהורט Q1/16 בערוץ הישיר, לא אחראים לבדם לתקבולים של $85 מיליון דולר שהניב אותו קוהורט עד דצמבר 2018 -- גם פרסומות המותג [לאחר היווצרות הקוהורט] גורמות לחברי הקוהורט להפוך למנויים משלמים (וכך גם מיילים המפצירים במשתמשים רשומים להפוך למנויים משלמים).

בעייה ראשונה -- כותרות ואי גילוי מונה ומכנה

פייבר הגישה ל-SEC טיוטה ראשונה ב-1 בפברואר 2019. ליד הגרף הופיעה המשפט הבא:

האם אתם מזהים בעיה בניסוח המשפט הזה? הנה הערות סגל ה-SEC לגרף ולמלל סביבו בטיוטת התשקיף הראשונה:

3. Please revise your disclosures to address the following as it relates to your discussion of time to return on investment.

-

· How marketing expense applicable to new user acquisitions is determined;

-

· To the extent that the information used in this calculation is not based on GAAP information, indicate as such and explain how the calculations differ from GAAP;

-

· Provide comparable information for another cohort period or clarify that the cohort information may not be representative of every year; and

-

· Tell us whether management uses this information in managing your business or assessing performance.

אז הבולט הראשון מבקש מפייבר להבהיר אילו סוגי marketing expense נכנסים למכנה של יחס היעילות tROI. ההבהרה מתבקשת, בין השאר לאור המשפט הלא מוצלח שאמר כי tROI מודד את מספר החודשים שלוקח להחזיר את כול ה-marketing expenses. הנה כך תיקנה פייבר את המשפט הלא מוצלח בטיוטת התשקיף השנייה:

| טיוטה שנייה | טיוטה ראשונה |

|---|---|

| We measure the efficiency of our buyer acquisition strategy by Time to Return On Investment ("tROI"), which represents the number of months required for us to recover performance marketing investments during a particular period of time from the revenue generated by the new buyers acquired during that period. | We measure the efficiency of our buyer strategy by Time to Return On Investment ("tROI"), which represents the number of months required for us to recover marketing expenses on new user acquisition during a particular period of time from the revenue generated by the new buyers acquired during that period. |

| Performance marketing investments in new buyer acquisition is determined by aggregating online advertising spend across various channels, including SEO, SEM, video and social media used for buyer acquisition. | הפסקה מימין חדשה לגמרי |

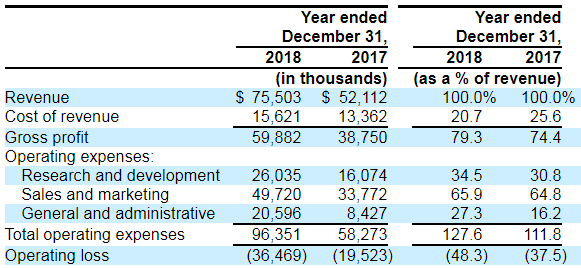

העניין בסוגי וסכומי ההוצאות במכנה ה-tROI חשוב למשקיע סביר כיוון שהוצאות השיווק והפרסום של פייבר גבוהות מאד יחסית להכנסות (כ-66% בשנת 2018):

את הבולט השני, אפשר להבין כבקשה להראות את הקשר הכמותי בין הסכום במכנה ה-tROI לבין סכום הוצאות שיווק ופרסום בדוח רווח והפסד. הנהלת פייבר לא הבינה זאת כך (התשובה המלאה כאן):

The GAAP and non-GAAP expense on performance marketing investments are the same.

The Company respectfully acknowledges the Staff’s comment and has added 2018 quarterly cohorts to the chart on page 61. The chart now includes the cumulative revenue to performance marketing investment ratios for all past eight quarterly cohorts as of December 31, 2018.

The Company’s management closely monitors, tracks and manages marketing efficiency on a quarterly basis. tROI and cumulative revenue to performance marketing investment ratios reflect short-term and long-term marketing efficiency, respectively.

ישאל השואל: מדוע בתשובה לסגל ה-SEC מדגישה פייבר כי המכנה ביחס tROI לא כולל עלויות פרסום חוצות (גוגל: fiverr ads subway), אבל בטיוטת התשקיף היא לא מציינת עובדה זאת במפורש? מה? היא חושבת שהציבור בכללותו יותר מתוחכם מסגל ה-SEC?

בסבב ההערות השני, הגיב סגל ה-SEC ב-28.3.2019 (כאן), כלהלן:

3. We note your response to our prior comment 3. Please also address the following:

-

· Clarify what the acronyms SEO and SEM stand for in your definition of performance marketing investments.

-

· Revise to explain that the marketing expenses used to calculate tROI exclude out of home advertising and describe the other excluded fixed costs.

-

· Explain why certain costs are excluded from your performance marketing investments and related tROI calculations.

-

· Clarify that the marketing expense used in this calculation is not the same as marketing expense determined under US GAAP for the purposes of income statement classification.

-

· Disclose whether there are any limitations on the use of the metric.

-

ההערה הרביעית דורשת לציין בסמוך לגרף, ברחל בתך הקטנה, כי המכנה של tROI אינו סך הוצאות שיווק ומכירה בדוח רווח והפסד וההערה השניה דורשת לציין ספציפית שהוא אינו כולל עלויות פרסום חוצות.

בסופו של יום, התשקיף הסופי כולל את הגילוי הבא מתחת לגרף:

סגל ה-SEC, אם כך, טיפל היטב בצד האיכותני של הגילוי. אבל מה קורה עם גילוי כמותי למכנה של tROI, גילוי שוויקס נותנת על גבי השקף. ובכן, אין גילוי כזה. ה-MD&A בתשקיף הסופי מגלה רק בכמה גדלה ההוצאה בגין performance marketing אבל לא את סכומה האבסולוטי:

האם מתוך הגילוי שפרפורמנס מרקטינג אחראי לשני שליש מהגידול בהוצאות שיווק ומכירה אני אמור לשער שהוצאות פרמפורמנס מרקטינג הם שני שליש מסך הוצאות שיווק ופרסום? לדעתי, סגל ה-SEC כשל בכך שלא דרש גילוי מפורש לסכום האבסולוטי בדומה לדרישה שהוציא לאובר וליפט (עליה כתבתי כאן).

אפשר אם כך לומר ביחס לגילוי הכמותי למכנה ה-tROI: פייבר לא מגלה בתשקיף את מה שוויקס מגלה וולנטרית במצגות.

בעייה שנייה ושלישית -- הסוגיות האנליטיות

בהערות הסבב השני בבולט השלישי והחמישי לעיל, מבקש סגל ה-SEC הסבר מדוע חלק מהוצאות השיווק (כגון עלות פרסום חוצות) מוחרג ממכנה ה-tROI וגילוי על "מגבלות בשימוש" ביחס הזה (כנראה לאור אופן מדידת המכנה, כאמור).

להלן תשובת פייבר (כאן).

התשובה מסווגת עלויות שיווק ומכירה ל"משתנות וישירות" מצד אחד ול"קבועות" מצד שני. לטעמי, המענה הזה לא נותן תשובה לבעייה השנייה והשלישית. לשיפוטכן. ובמאמר מוסגר, לא ברור לי איך לסווג עלות שכר עובדים העוסקים ב-SEO (גוגל: "in house" SEO costs). מצד אחד פייבר כתבה שעלויות SEO כלולות בפרמורמנס מרקטינג ומצד שני היא כתבה ששכר עובדים לא כלול בפרמורמנס מרקטינג. אז?

בכל אופן, פייבר הוסיפה לתשקיף את הגילוי הבא באופן בולט מתחת לגרף, שבין השאר מזהיר את קוראי התשקיף מהתעלמות מעלויות שיווק ומכירה שאינן במכנה ה-tROI:

במכתב ההערות השני, ה-SEC הוסיף עוד הערה (בהשוואה למכתב הראשון) הממוקדת בבעייה השלישית (שכאמור לדעתי היא נכונה לגבי מצגות וויקס). הנה ההערה והמענה:

4. The chart presented on page 61 appears to compare the cumulative revenue for a specific cohort period to the performance marketing investments made during the initial cohort period. Please clarify whether any additional marketing costs are incurred in subsequent periods to maintain and grow the cohort group, and if so, explain how such costs are factored into your analysis. To the extent subsequent marketing costs are excluded from your analysis, please explain why.

Response: The Company respectfully acknowledges the Staff’s comment and advises the Staff that there are no material subsequent marketing costs incurred to maintain and grow the cohort group.

כפי שכבר הסברתי, פרסומות מותג לאחר יצירת הקוהורט תורמות משמעותית להכנסות מהקוהורט. כך, שאני לא מרגיש בנוח עם המענה. שימו לב, שהמענה "מנצל" לכאורה אי-דיוק לשוני לכאורה בהערת ה-SEC שבמקום לשאול אם הפרסומות מביאות לגידול ההכנסות מהקוהורט הוא שאל אם הן מביאות לגידול בקוהורט עצמו.

פייבר הוסיפה לתשקיף את המשפט:

כאמור, המשפט נכון טריבייאלית מבחינה טכנית. השאלה שלא ניתן לה מענה היא האם הוצאות הפרסום לאחר יצירת הקוהורט תורמות לתחזוק וגידול ההכנסות מהקוהורט.

וכך אנו מגיעים למכתב ההערות השלישי של ה-SEC, שחותם את הדיון עם בקשה לגילוי הצהרתי שההנהלה עושה ב-tROI שימוש יום יומי פעיל לקבלת החלטות תפעוליות ובבקשה לדסקס מדוע החלטות על הוצאות שיווק "קבועות" שהוחרגו ממכנה היחס מתקבלות בנפרד (כאן ההערה והמענה):

2. We note your response to prior comment 3. Please revise your disclosures to indicate that tROI is actively used by management in making day-to-day operational decisions, and include a discussion of why fixed costs are considered separately from performance marketing investments in the tROI calculation...

Response: The Company respectfully acknowledges the Staff’s comment and will add the following underlined disclosure on page 61:

Our performance marketing investment has limitations as an analytical tool, including that it does not reflect certain expenditures necessary to the operation of our business, and should not be considered in isolation. Certain fixed costs are excluded from performance marketing investments and related tROl calculations because performance marketing investments represent our direct variable costs related to buyer acquisition and its corresponding revenue generation. tROl measures the efficiency of such variable marketing investments and is an indicator actively used by management to make day-to-day operational decisions. ...

אז במה הועילו הערות ה-SEC למשקיע הסביר המעיין בתשקיף?

א. הן גרמו להוספת גילוי בולט ליד הגרף האומר כי מכנה ה-tROI מחסיר עלויות שיווק ופרסום הנדרשות לתפעול העסק. ללא הגילוי הזה, הגרף היה עלול להיחשב, רחחמנא לצלן, כגילוי העשוי להטעות.

ב. גם הגילוי הנוסף וגם התכתובת -- שהיא חלק ממכלול הגילוי למשקיע -- חושפת בפני המשקיע כי השימוש האנליטי ביחס tROI מוגבל, שנוי במחלוקת וכו' ואת הסיבות למוגבלות זו.

כאמור, התאכזבתי שסגל ה-SEC לא דרש גילוי כמותי להפרש בין מכנה ה-tROI לבין הוצאות שיווק ומכירה בדוח רווח והפסד -- גילוי שהיה מאפשר לאנליסט לחשב tROI עם מכנה המוגדר אחרת.

פוסט זה משויך לקטגוריה "תכתובות SEC".

תגיות לפוסט זה: Fiverr | WIX | קוהורטים cohorts |