לאחרונה נתקלתי בהערה הבאה שהעביר סגל ה-SEC לטאבולה לקראת מיזוגה עם SPAC:

"Your presentation of the non-GAAP performance measure called “ex-TAC Revenues” appears to adjust GAAP revenues recognized on a gross basis to exclude traffic acquisition costs and thus present revenues as if they were recognized on a net basis. Please explain to us why you believe this non-GAAP measure does not substitute individually tailored revenue recognition and measurement methods for those of GAAP. Refer to Question 100.04 of Compliance and Disclosure Interpretations on Non-GAAP Financial Measures and Rule 100(b) of Regulation G."

ההערה הזו בעייתית, משום שההנחיה המכונה "Question 100.04", שאליה מפנה הסגל בהערתו אינה רלבנטית לטענה שמעלה סגל ה-SEC כלפי טאבולה, הנסחרת כעת בנסדאק כ"חברה זרה" ישראלית (כלומר מפרסמת דוחות שנתיים על גבי טופס 20-F ומפרסמת תוצאות רבעוניות בהודעות לעיתונות המצורפות לטופס 6-K).

כדי להבין מדוע ההערה הזו לטאבולה שגויה צריך להבין את "Question 100.04", שבאה לעולם בעקבות הערה נכונה שנתן סגל ה-SEC לחברה זרה ישראלית אחרת: וויקס.

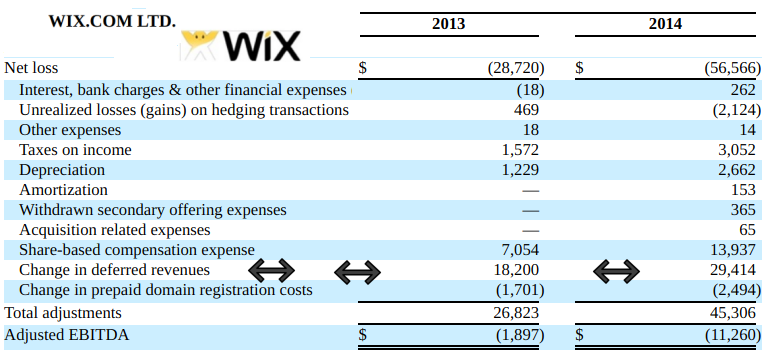

סגל ה-SEC העביר לוויקס את ההערה ב-5 ינואר 2016 והיא מתייחסת להתאמת הנונ-גאאפ הבאה שנכללה בדוח השנתי של וויקס לשנת 2014 על גבי טופס 20-F:

וזו לשון ההערה:

"We note your disclosure of “Adjusted EBITDA” which includes adjustments for the changes in deferred revenues and prepaid domain registration costs. Your calculation of “Adjusted EBITDA” begins with “Net loss” which implies that “Adjusted EBITDA” is a performance measure; however your disclosure that the measure is “used to evaluate the cash profitability of the business” is not consistent with that of a performance measure since the deferred revenue has not been earned. Please tell us the appropriateness of this measure as a performance measure and how it is useful to investors."

בהתאמה הזו, המזניקה את ה-EBITDA המותאמת כלפי מעלה בסכום השווה לגידול ביתרת "הכנסות נדחות", וויקס מחליפה למעשה את שיטת GAAP להכרה בהכנסה בגין מתן שרותים למנוי ששילם מראש (הכרה בהדרגה לאורך תקופת המנוי) בשיטה המכירה במלוא דמי המנוי ששולמו מראש כהכנסה במועד קבלת דמי המנוי.

הערת ה-SEC מוצדקת לחלוטין. מטרת הצגת מדד ביצוע נונ-גאאפ היא לשפר את ההשוואה בין הביצועים בתקופה הנוכחית לביצועים בתקופה מקבילה. על כן, התאמות למדד כזה צריכות להיות מגבלות לניטרול הוצאות או הכנסות הנושאות אופי חד פעמי. זו לא טבעה של ההתאמה שה-SEC מבקש לחדול ממנה.

התשובה של וויקס לא סיפקה את הסגל, והוא חזר לוויקס עם ההערה הבאה ב-16 בפברואר:

"You acknowledge that the revenue used in your non-GAAP measure is not earned. However, you refer to the measure as adjusted "earnings" before interest, taxes, depreciation, and amortization. Please tell us why you believe that a measure that is inconsistent with the concept of earnings should be identified using that term."

בתשובתה, הציעה וויקס ל-SEC פשרה. ה-SEC לא השיב להצעה וסגר את ההתכתבות ב-28 במרץ.

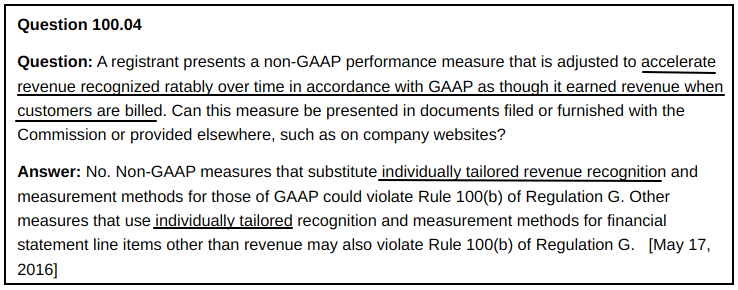

ואז ב-17 במאי, פרסם ה-SEC הנחית איסור כללית על שימוש בהתאמה מהסוג שאת השימוש בה ביקש להפסיק אצל וויקס:

שנה שלמה לאחר פרסום ההנחיה, ב-5 ביוני 2017, שוב פנה סגל ה-SEC לוויקס. הפעם, מצויד ב-"Question 100.04", הוא ביקש ממנה לחדול מהצגת ההתאמה הזו בטבלאות המוצגות באתר קשרי המשקיעים:

"In the Investor Relations section of your website, you have posted earnings slides, supplemental data, and shareholder update presentations that include a measure of nonGAAP gross profit, calculated as non-GAAP gross profit plus change in deferred revenues, less deferred domain expenses. We believe the presentation of a performance measure that substitutes individually tailored revenue recognition and measurement methods for those of GAAP violates Rule 100(b) of Regulation G. Refer to Question 100.04 of the Non-GAAP Compliance and Disclosure Interpretations issued on May 17, 2016. Please remove these measures from future public presentations. "

וויקס נענתה לבקשה. וויקס נענתה לבקשה. (על הערת ה-SEC לטאבולה הנסמכת בשגגה על Question 100.04, ראו כאן.)

פוסט זה משויך לקטגוריה "

non-GAAP Metrics | מדדי נונ-גאאפ".

תגיות לפוסט זה: